Economic Policy - Options and Task Allocation

Historical archive

Published under: Bondevik's 2nd Government

Publisher: Ministry of Finance

Address to the Foreign Exchange Seminar of the Association of Norwegian Economists at Gausdal on 29 January 2003

Speech/statement | Date: 29/01/2003

The Minister of Finance, Per-Kristian Foss, address to the Foreign Exchange Seminar of the Association of Norwegian Economists at Gausdal on 29 January 2003 (29.01.2003)

Subject to changes

Per-Kristian Foss, Minister of Finance

Address to the Foreign Exchange Seminar of the Association of Norwegian Economists at Gausdal on 29 January 2003

Economic Policy - Options and Task Allocation

1 Introduction

Norway is a wealthy country. The main reason for our wealth is that we put our resources to good use. We benefit from a highly educated and competent labour force a well-functioning business sector. Moreover, nature has blessed us with bountiful resources.

However, herein lies a danger: We may easily come to imagine that we are absolutely unique, and that we may therefore defy some of the economic laws of gravity. We create the impression of a country ”flowing with milk and honey” or having won the lottery! It is correct that Norway is a very good country in which to live. I need not examine any UN statistics to know that - we experience it ourselves every day.

But statistics and surveys only tell us how we were doing yesterday. They do not tell us how things are today, and much less do they reveal what tomorrow will bring.

The challenge is to make Norway a good country to live in - in the future.

The IMF paid Norway another visit just before Christmas. We were awarded good marks on our economic policies, whilst being reminded that abundance breeds complacency. We cannot survive on oil alone. We will first and foremost have to live off the values we create. In fact, the value of our manpower is 15 times that of our oil and gas - including both what we have extracted and allocated to the Petroleum Fund and what remains beneath the seabed.

2 Challenges Facing Sector Exposed to Competition

The challenges now facing manufacturing industry and industries exposed to foreign competition highlight the importance of a gradual and cautious approach to the use of oil revenues.

There is no doubt that parts of the industries exposed to competition are now struggling. This may be caused by

- weakened demand abroad;

- domestic cost increases, reflecting, amongst other things, costly wage settlements;

- a high rate of interest; and

- a stronger Norwegian krone exchange rate.

This may bring on large and abrupt changes. Change is part of the everyday life of businesses. Consequently, it is not in itself negative that some jobs vanish or that businesses have to renew themselves. The danger, however, is that existing jobs may disappear faster than new ones are created.

The Norwegian krone exchange rate has over the last two years firmed by a total of almost 13 percent, when measured as the effective trade wheighted krone exchange rate . The krone has not been stronger since the mid-1980s.

The competitiveness of Norwegian trade and industry has suffered severely under the wage settlement and the exchange rate of the krone. The hourly wage costs of workers in Norwegian manufacturing industry are now more than 30 percent higher than those of our trading partners.

Well-functioning wage determination is important in ensuring, over time, low unemployment as well as a sound business sector capable of growth. The negotiation of each pay settlement remains the responsibility of the social partners, but it is important for us to have a joint understanding of the challenges facing the Norwegian economy.

The 2003 wage settlement needs to be better fit to what the Norwegian economy can sustain, than was the case last year. Government has by way of the incomes policy cooperation taken measures to contribute to that. Last week’s joint declaration from the Liaison Committee, where the heads of all major trade unions and employer’s organisations meet Government, is a step in the right direction. Therein was signalled that the 2003 wage growth should be adapted to what may be tolerable for the sector exposed to competition, to enable wage growth to decline towards the rate of our trading partners. If this is materialised, we will have broken a several year long trend of excessive wage growth and impaired competitiveness.

3 On Economic Policy Task Allocation

New Norwegian fiscal and monetary policy guidelines were introduced in March 2001. The oil revenue spending rule was put into effect, and the Norges Bank was provided with new monetary policy guidelines. It may be useful to briefly summarise the scope of the said changes.

The fiscal rule offered us a clear strategy as to the amount of oil revenues to be spent via the Fiscal Budget each year. Previously we had no such strategy. This did not mean that one then refrained from spending oil revenues on the contrary.

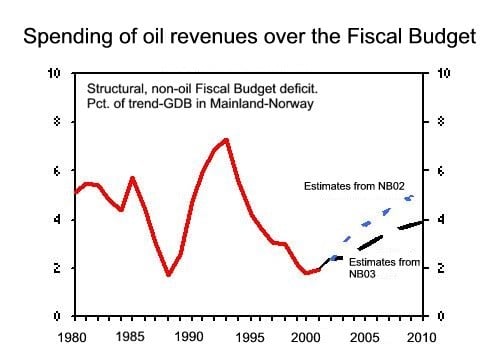

The diagram shows the historic and projected non-oil structural budget deficit. Under the spending rule this indicator shall correspond to 4 percent of the Petroleum Fund capital as of the beginning of the fiscal year. The diagram shows the oil revenue spending trajectory as estimated in this year’s National Budget (NB03). In the diagram this is compared to the estimates from last year’s National Budget (NB02).

The diagram illustrates some important insights:

First of all, there was no regime change in terms of the actual spending of oil revenue via the Fiscal Budget in March 2001. We spent more oil revenue via the Fiscal Budget practically every year during the 1980s and 1990s than we intend to spend in coming years.

The innovation is that now we have a clear strategy as to the amount of oil revenue we should spend - previously there was no such strategy. And the strategy is that oil revenue spending shall be determined by the real return on Petroleum Fund capital. This is sensible in view of the very strong growth in pension expenditure which we know will materialise over coming decades.

Secondly, future year-on-year changes in oil revenue spending are much smaller than what has been experienced in the past. This implies that fiscal policy will to a lesser degree be used actively to stabilise the economy.

This has monetary policy implications to which I will return later.

Thirdly, the diagram illustrates that the coming increase in oil revenue spending is, after all, quite limited. The projections suggest that by 2010 we will have increased spending by approximately 2 percent of mainland Norway GNP. Of course, 20 - 25 billion kroner is a lot of money in the context of tight government budgets, but the structural changes to the economy as a result of this are limited.

The Ministry of Finance has repeatedly stated that the impairment of competitiveness - or the so-called real appreciation - we have experienced since March 2001, is excessive when compared to the planned oil revenue spending increases. In last autumn’s National Budget we presented figures that might suggest real appreciation in the region of 4 - 8 percent for the period until 2010 as a whole. Over the last two years we have seen real appreciation of some 17 percent.

There may of course be other reasons for the strong appreciation of the krone. However, we are under the impression that many market players have overestimated the amount and importance of the increased oil revenue spending. The same applies to the wage negotiation parties. The aggregate result of this may have been a significant overshooting of the exchange rate.

The need for real appreciation will also depend on how the increased oil revenue spending is used. If the entire oil revenue spending increase is dedicated to the reduction of direct and indirect taxes, the National Budget calculations suggest that the required real appreciation will not be more than 3 - 4 percent by 2010.

Looking back at what has actually happened, direct and indirect taxes have been reduced by more than 19 billion kroner over two years. The real oil revenue spending increase over the same two year period is approximately 7 billion kroner.

Taking this Storting term as a whole (2001-2005), the Government has in the Sem declaration committed itself to tax reductions exceeding the increase in oil revenue-spending.

Consequently, the need for real appreciation of the krone is rather limited. This reinforces the impression of an overreaction in the exchange rate market.

The monetary policyinflation target was the other new measure introduced the March 2001 economic policy guidelines. It was explicitly stated that monetary policy shall aim for approximately 2^2 percent inflation over time.

The inflation target is motivated by a need for a nominal anchor clarifying the role of monetary policy in supporting stable economic development. The operational target is inflation-related. Low and stable inflation is of importance for ensuring stable production and employment, and will also contribute to stabilising exchange rate expectations over time.

At the same time we need to be prepared for greater krone exchange rate fluctuations than in the past - in line with the experience of other small countries with floating exchange rates.

The recent appreciation of the krone exchange rate has been very steep, and a number of commentators have expressed concern for the situation of the industries exposed to international competition. I share this concern. As mentioned, I believe that markets have overreacted to the policy changes. A 2^2 percent inflation target is ^2 percentage point higher than the expected inflation of our trading partners. Consequently, there should over time be no need for nominal appreciation of the krone exchange rate in order to achieve the required real appreciation.

The krone exchange rate appreciation over the last couple of years has to be seen in the context of the Norwegian economy being regarded as strong relative to the situation in other countries. The OECD economies have been characterised by low growth and increasing unemployment. One has sought to counteract this by way of monetary policy, and international interest rates are therefore at a very low level in historical terms.

Norway has experienced a completely different stage of the economic cycle. We have seen high capacity utilisation and low unemployment. At the same time oil prices have remained high. A firm labour market yielded strong wage growth in 2002, well ahead of what is compatible with the inflation target. The high wage growth has resulted in the Norges Bank keeping Norwegian interest rates at a high level, and markedly above the international interest rate level.

The high interest differential relative to other countries is probably a main explanatory factor of the appreciation of the krone.

Moreover, the Norwegian krone may have been perceived as a ”safe haven”, especially against a background of turbulent financial markets and international tension. In a period of high share market volatility many investors will wish to reallocate their portfolios. Norwegian krone investments will then appear attractive due to the relatively high rate of interest. Such portfolio adjustments contribute to the appreciation of the krone. Such developments may be reversed upon a recovery in the share markets and a reduction in the differential between Norwegian and international interest rates.

There may also be an element of the krone having by some been considered a ”petro-currency”. The oil price has been high as of late. We cannot rule out the Middle East situation resulting in another significant oil price hike. Neither can we rule out a marked decline in the oil price. High oil prices favour the Norwegian economy, but have a negative effect on our trading partners.

A significant oil price increase may contribute to the krone remaining strong. On the other hand, the Petroleum Fund ensures that high oil prices are mainly reflected in increased fund allocations, and not in increased demand in the Norwegian economy. This dampens the impact of high oil prices on the krone exchange rate. At the same time, the Petroleum Fund capital allows us to maintain fiscal policy in the event of a considerable drop in the oil price.

Consequently, the creation of the Petroleum Fund in 1990 makes the Norwegian economy significantly less vulnerable to oil price fluctuations now than what was the case in the 1980s. Moreover, oil revenue spending via the Fiscal Budget is materially lower than in the mid-1980s, as illustrated by the earlier diagram. Furthermore, the investment plans of oil companies probably remain robust under the assumption of oil prices below 15 dollars per barrel - that was not the case during the 1980s’ oil price contraction.

Through autumn and winter we have observed strong indications of a cyclical downturn in Norway. International growth, on the other hand, appears likely to remain weak for some time. Nevertheless, in the longer term there is reason to expect Norwegian and trading partner economic cycles to be more in tune with each other than what has been experienced over the last few years. This will contribute to Norwegian interest rates becoming better aligned with interest rate levels abroad. However, this is conditional upon a significant reduction in Norwegian wage growth when compared to the levels of recent years. Foreign exchange market conditions may then become normalised. The exact mechanisms which have this far firmed the krone, may then contribute to a softening of the krone exchange rate.

There is, however, considerable uncertainty. Should expectations of the krone exhange rate remaining strong over a relatively long term become entrenched, there may be a danger of the downscaling of the sector exposed to competition taking place too rapidly. Such a scenario may yield weaker Norwegian economic growth than previously estimated.

The new economic policy guidelines amount to a material realignment of economic policy task allocation. The fiscal rule offers a medium term fiscal policy benchmark. Monetary policy, at the same time, has been charged with a clear responsibility for contributing to a stabilisation of production and employment developments.

Based on its wage and price projections, the Norges Bank last year conducted a tight monetary policy featuring high interest rates. This has in conjunction with low interest rates abroad contributed to the appreciation of the krone exchange rate. The economic policy guidelines imply that in case of a cyclical downturn, and provided that estimated inflation is consistent with the inflation target, the Norges Bank will reduce the interest rate. The interest rate was reduced by 1 percentage point during December and January. Concurrently, it has been indicated that there is an increased probability of an inflation rate of less than 2^2 percent over a two year time horizon.

4 Measures Enhancing the Growth Potenital

Developments in terms of competitiveness, interest rates, krone exchange rates and all other important indicators depend not only on the initiatives taken by the Norges Bank, the Storting or the Ministry of Finance. We must all, both in the private and public sectors, ensure that every single krone is put to the best possible use from day to day.

The challenge facing each business and industry is improving competitiveness by outperforming competitors in terms of productivity growth, and developing new ideas and profitable businesses.

The main role of the State is to facilitate this by way of an efficient public sector and a general framework that is conducive to industry and commerce, in order for Norway to retain and attract profitable business activity and benefit from good access to manpower.

This is well in keeping with the Lisbon Strategy adopted by the EU in March 2000. The main objective of the Lisbon strategy is to improve the EU countries’ competitiveness by creating a framework that contributes to improved efficiency and resource utilisation within the EU common market. At the core of ongoing follow-up are increased employment, structural and economic reforms within the financial, energy and transportation markets and enhanced knowledge investment.

Norwegian trade and industry are used to striving to stay ”ahead of the class”. That is both natural and necessary for a small country with an open economy. EU and EEA enlargement through the admission of 10 new countries opens up exciting prospects for trade and industry, whilst posing challenges.

Not only must each individual business continue to stay ahead of its competitors. Government also needs to focus on competitiveness in designing the education system and in formulating industrial and structural policies. The objective is to ensure a general framework offering a sound basis for high economic growth and improved welfare.

For purposes of improving the efficiency of the overall economy, Government emphasises:

- Modernising the public sector to improve productivity, quality and user friendliness, and channelling resources to those areas where they are needed the most.

- Reducing the tax level and developing the most efficient and neutral tax system feasible.

- Ensuring efficient resource utilisation through effective competition.

- Designing a comprehensive innovation policy attaching weight to quality in education and research

Modernising and increasing the efficiency of the public sector is one of our main challenges. This is for a simple reason - we cannot in coming years expect the same labour force growth we have had in the past.

If we want more and better public services, we will have to either channel manpower away from the private sector or to improve the organisation of such public services. The former should be avoided – as it would impair trade and industry. Consequently, we will have to do the latter.

That requires us to improve public sector resource utilisation.

The Norwegian public sector is large relative to the overall economic activity. The number of public sector employees has increased by approximately 125,000 persons over the last decade. Public expenditure amounts to some 40 percent of overall GDP. Consequently, the efficiency of publicly financed service provision and systems for transferring resources is of major importance to overall welfare.

Moreover, the public sector must offer efficient services that are adapted to user needs, that are easy to access and that do not entail unnecessary extra work on the part of users.

Government has therefore implemented a public sector modernisation programme. Important features of the programme are:

- Reform efforts will be based on decentralisation and delegation.

- Governmental service providers will be granted more independence, and the municipalities will be granted more freedom.

- Public service users will be granted more freedom of choice, and resource allocation will to a greater extent reflect user preferences.

- Improved service provision efficiency and quality will, amongst other things, be effected by way of increased competition. Competition from private providers will be enhanced.

- The distinction between public administration and service provision will be reinforced. The fox shall not mind the geese.

Another important feature of Government economic policy is reducing the level of direct and indirect taxes. The objective is to provide a sounder basis for sustained economic growth.

We have already implemented significant tax reductions. Some examples are the phasing out of the investment tax, the abolition of the unilateral dividend tax, the removal of the air passenger duty, the improvement of depreciation rates, the rescission of import tariffs on manufactured goods and the introduction of R&D expense tax credits.

Equally important as the tax level itself is the design of the tax system as such. In 2001 Government appointed a government expert committee chaired by former Minister of Finance Arne Skauge. The committee is to submit its recommendations in early February.

The committee has been charged with designing income and wealth taxation, taking regard of efficient resource utilisation, distribution issues and simplicity. Furthermore, the committee will consider whether the system of direct and indirect taxation sufficiently accommodates increased international capital and labour mobility. The committee will consider measures that may reduce the differential between marginal tax rates on earned and unearned income, changes to wealth taxation and changes that may contribute to increased stability and predictability of the system of direct and indirect taxation.

In January 2002 Government appointed a committee chaired by professor Jørn Rattsø and charged with assessing measures to minimise the impact of VAT on municipalities’ decisions on whether to purchase services from private providers or produce them themselves. The committee submitted its recommendations in December 2002. The committee suggests a general VAT compensation scheme for the municipal sector. Interested parties have been invited to submit comments on these recommendations. Government will follow up on the work of the committee as swiftly as possible, and aims to submit a proposal to the Storting in next autumn’s Fiscal Budget, with a view of implementation at the turn of the year.

Competition policy forms an important part of trade and industry policy aimed at safeguarding flexible markets and improving the scope for reorganisation. Well-designed regulations and effective supervision preparing the ground for real competition are important.

Government adopted a competition policy action plan in November 2001, for purposes of reinforcing competition policy. The five main principles of the plan are:

- More weight attached to competition policy considerations and strengthening of the Norwegian Competition Authority.

- Reviewing government regulations and schemes that may impede competition.

- Ensuring that public procurement contributes to stimulating competition and offering scope for start-ups.

- Ensuring that the disposal of government-owned companies does not contribute to competition impediments and monopolisation tendencies.

- Seeing to it that public sector activities are organised and operated in a manner conducive to competition.

Recent research, amongst others in the OECD, suggest that effective competition is important for ensuring maximum growth over time. However, the ability to generate economic growth through invention and innovation also depends on the overall innovation policy. This requires a commitment to education, research and development. The State will contribute to this, but primary responsibility for innovation and reorganisation lies with each individual business.

The will to develop something new or to start a new business depends on more than regulations and subsidy schemes. An entrepreneurial spirit amongst ordinary people is required, and this is a matter of culture. Norway has generated many capable entrepreneurs. Just before Christmas a survey showed that Norway ranks amongst the top of the European business start-up league. Only Ireland and Iceland are ahead of us amongst the European participant countries. The survey shows that a lack of ideas is not what impedes start-ups in this country. The problem is insufficient qualifications.

A large part of the answer to developing a stronger entrepreneurship culture in Norway lies with the businesses themselves. But the schools can also contribute. How can the schools become better at developing qualifications and attitudes of importance to innovation in business and society? Children should learn more, be allowed to express themselves creatively, dare to accept challenges, and draw on their creative abilities. Only such a school will equip us to face the need for change and creative power in business and society. Attitudes adopted at an early age are carried into adult life.

No one starts a business to fill out forms and shift documents. We want it to become simpler to start a new business. This Government cuts red tape and simplifies the regulations applicable to businesses. Thus far the Business Acquisition Act and 420 Regulations have been abolished. Proposed simplifications to the Planning and Building Act have been submitted to the Storting. The phasing-out of the investment tax also prepared the ground for the removal of 15 Regulations. In October the Minister of Trade and Industry presented an action plan for “A simpler Norway”, with a total of 122 measures to simplify life for trade and industry.

5 Conclusion

This Government is committed to an economic policy offering improved scope for operating business activities in Norway. Tax reductions and numerous other measures have contributed to achieving this. Nevertheless, the strong krone means that, right now, this is not how many businesses within the sector exposed to international competition see things.

The strong krone represents the fallout from last years’ rather wayward wage settlement. Economic policy task allocation says that monetary policy is charged with bringing about the necessary realignment. The quicker this signal is acted upon by the social partners, the shorter will be the period characterised by a high interest rate and a strong krone.

Last week’s joint declaration of the social partners suggests that this lesson is in the process of being acknowledged. It then remains to hope that developments throughout the year will conform to the declared intention that a reduction in wage growth towards the level of our trading partners must be achieved. Lower wage growth is a basic prerequisite for avoiding the entrenchment of Norwegian unemployment at a higher level than we have been used to.

The Norwegian economy faces many challenges in 2003 and beyond. Fiscal policy, monetary policy and incomes policy have a heavy burden to shoulder. The new economic policy guidelines have now been in operation for almost two years. I believe we have put in place a good system characterised by a clear apportionment of responsibility. I believe it would be sensible of us to permit this system to remain in operation.

If we adopt a somewhat longer time horizon, it is primarily our ability to create value that will determine economic growth and welfare a few years ahead. Economic policy debate is largely focused on oscillations around a trend. However, the most important issue over time is how the trend develops. That is what determines the magnitude of economic growth.

This is why the tax system modifications soon to be proposed by the Skauge Committee are important. And this is why it is important that we stand by what we said in the Sem declaration as regards continued reduction of direct and indirect taxes. At the same time we have to strive, across all other areas, to facilitate trade and industry innovation and growth.